Investment Strategy: Driving Through Fog

Summary: Driving in a heavy fog is difficult, frightening and exhausting, as every investor knows today. Slow down, be defensive, and keep moving forward.

There’s No Turning Back

I have experience driving in heavy fog. Some years ago, we lived in Lake Arrowhead. There was only one way to get there, a 26 mile drive up the mountain on “Rim of the World Drive,” a steep, narrow road carved out of the side of a mountain with sheer drop-offs to the valley below. Scary enough on a sunny day. Petrifying late at night in heavy fog.

Once you’re in it, there is no turning back. You can’t see far enough to turn around. You are afraid to go forward lest you stray from the road and drive off the cliff. You are afraid to stop for fear that another car will hit you from behind. So, you crawl ahead, holding the driver’s door open just enough to see the white center line you are tracking to make sure you are still on the road, hoping for the best, and vowing never to get into that situation again.

Sound familiar? I have been following the economy and financial markets for half a century as an economist, an investor, and a business owner. I have never seen a political and economic fog as thick as the one we are in today. I yearn for the good old days when all we had to worry about were the trade war, Brexit, and overpriced financial markets. Now we have a global pandemic, the sharpest drop in output in the last century, a series of multi-trillion-dollar rescue packages, a $3 trillion budget deficit, government debt that has, for the first time since World War II, exceeded GDP, and a central bank that has all-but nationalized the bond market. We are 3 weeks from an election with fake-militia vigilante groups threatening to disrupt the voting. There is still a trade war. Financial markets are even more overpriced.

Investors everywhere are looking for solid ground to stand on so they can make decisions about their portfolios. Just like driving in a fog, doing nothing is not an option. Every dollar in a portfolio must be held in assets denominated in some currency, within some asset class, with exposure to many risks. Here are a few thoughts on how to manage our way through the fog so that a year or two into the future, when we can see down the road again, we will be able to take advantage of the opportunities in front of us.

Slow down. Be defensive. Keep moving.

The first step is to realize, and admit, that you can’t see far enough down the road to make major new investment decisions and that nobody else can do so either. We don’t know when there will be safe, effective vaccines of sufficient quantity to make most people feel comfortable going back to work and resuming normal activities, the necessary condition to returning employment and output to normal levels. Until we do, we will have no way of knowing how long the government rescue actions will continue, or their implications for the size of deficits and debt we will have to clean up. The biggest mistake we can make is to pretend that we have all the answers. That means we should slow down, be defensive, reduce risk, keep moving forward and do whatever is needed to protect the value of the assets we already own.

COVID and its Aftermath

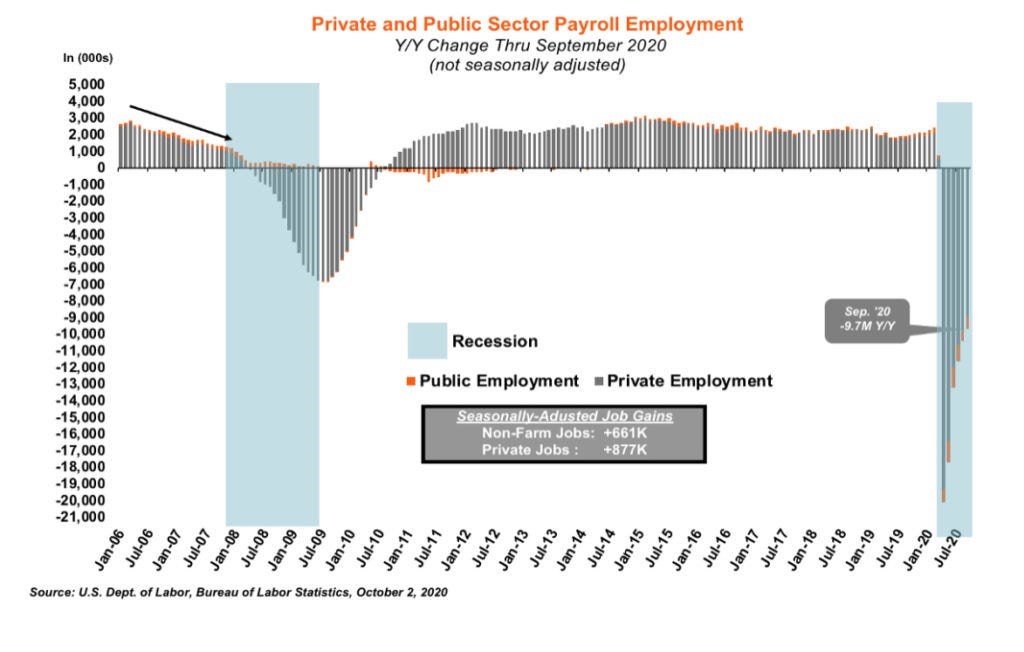

The first thing to understand about the impact of COVID on the economy is that it is not a recession and there won’t be a recovery, at least not in the normal sense. Those are words economists use to describe the periodic slowdowns in employment and output that happen when people, for one reason or another, slow down their spending. And it’s not a financial collapse like the subprime debt crisis we lived through just a decade ago. Instead, as shown in the chart, below, COVID has triggered an economy-wide work stoppage that happened because people are afraid to go to work.

The COVID pandemic’s impact on the economy is not much different than if there were a massive labor strike–a sharp drop in the number of people working, a sharp drop in our output of goods and services, shortages and rising prices of certain goods, and a sharp drop in spending as families tighten their belt to weather the storm until we are all working again. All of those have happened during COVID. The big difference between COVID and a labor strike is that there will be no quick ending. Instead of agreeing to a new contract and going back to work, the COVID economy will only improve when people, one at a time, feel that it is safe to go to work, to eat at restaurants, and to fly on airplanes again. That will not happen until there is a reason for doing so, which means a safe, effective vaccine, available to enough people so the risk of a person becoming infected while going about normal routines is negligible.

There is no chance at all of that happening this year. We should see progress in 2021 as vaccines are released and a growing portion of the population have had their arm jabbed. By the end of 2022, most of the people in the US and other rich countries who want it will have been vaccinated and we will have forgotten just how scared we all were. That makes 2023 the first year we should expect a more normal economy, with most people back to work and output humming along again.

Slow

Don’t be misled along the way by economic reports showing big growth rates. As you can see in the jobs chart, above, employment fell off a cliff in April and has been growing since but we are still almost 10,000,000 jobs in the hole for the year, almost double what we experienced at the worst of the last bust. It will take a lot of quarters of double-digit growth rates to repair this much damage.

Some of the damage will be permanent. We will eventually return to full employment but without the capital goods that we failed to produce during the pandemic. So, full employment output will be lower than it would have otherwise been.

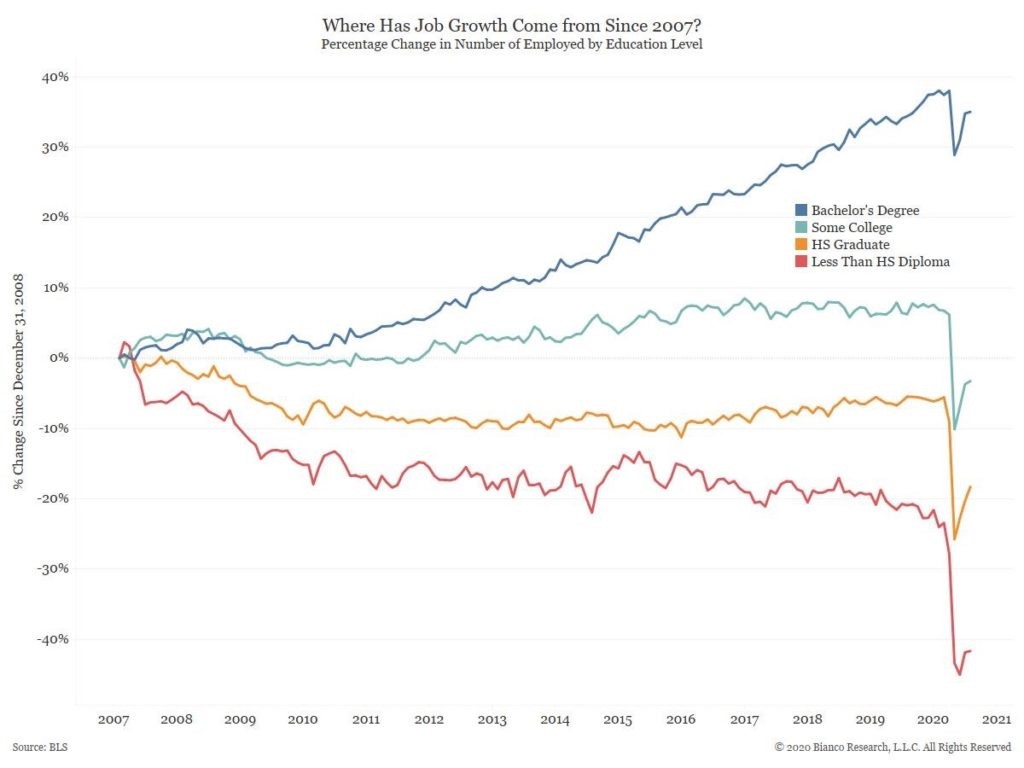

The COVID economy, of course, is not an equal opportunity disaster. Professionals have largely been able to work from home so not many job losses there. But, as you can see in the chart above, the COVID economy has not been as kind to everyone else. A chart showing job loss by income level, rather than education level, would show the same result.

Dr. John

The views and opinions expressed in this article are those of Dr. John Rutledge. Assumptions made in the analysis are not reflective of the position of any entity other than Dr. Rutledge’s. The information contained in this document does not constitute a solicitation, offer or recommendation to purchase or sell any particular security or investment product, or to engage in any particular strategy or in any transaction. You should not rely on any information contained herein in making a decision with respect to an investment. You should not construe the contents of this document as legal, business or tax advice and should consult with your own attorney, business advisor and tax advisor as to the legal, business, tax and related matters related hereto.