Bond Prices and Interest Rates

Yesterday, I posted a piece about inflation expectations and Treasury yields. I ended with a warning that long-term bonds, not stocks, are the riskiest assets in our portfolios today.

A good friend asked me to review some of the logic in more detail. Here you go:

1) The link between rising interest rates and falling bond prices is not just a theory that might or might not be true. It is the definition of an interest rate, or yield.

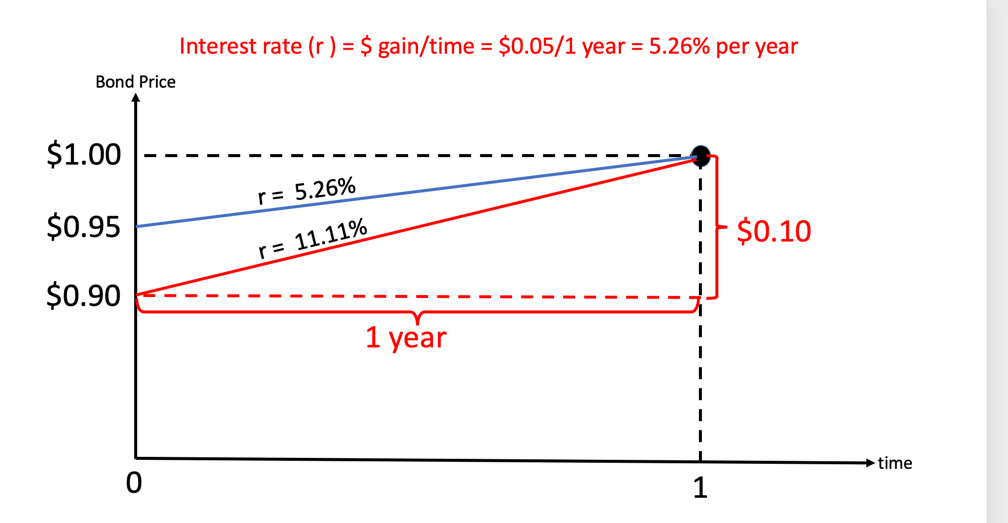

For example, In the chart below, if you pay the market price of $0.95 to buy a bond (an IOU) that promises to pay you $1.00 in one year then we would calculate its yield as r = ($100-$0.95)/$0.95 = $0.05/$0.95 = 5.26%.

If something changes in the marketplace and the market price of the same bond falls to $0.90, then we would calculate its yield to be r = ($1.00-$0.90)/$0.90 = $0.10/$0.90 = 11.11%.

So, saying that interest rates have gone up (in this case, from 5.26% TO 11.11%) is the EXACT SAME STATEMENT as saying that bond prices have gone down (in this case, from 95 cents to 90 cents).

2) the interest rate, or yield, (which is just a calculation we make by dividing a contractual interest payment by the price we pay for the security) on all sorts of assets rises and falls with inflation (actually, expected inflation). The best way to understand this is to think of the inflation rate as the “interest” you receive from owning a tangible asset like a house or a bar of gold. If you buy it for $100 this year and its prices goes up to $110 in one year (10% inflation) then the “yield” on the asset is $10/$100 = 10% (the increase in value divided by what you paid to buy it.)

The logic is, when inflation goes up, the “yield” on real goods goes up. That makes the yield on real goods high, i.e., more attractive, compared with the yield on bonds and other securities. That induces people to sell bonds to buy more houses and other hard assets to capture some of that extra yield, which pushes hard asset prices up and bond prices down. So, you don’t want to own bonds during riding inflation because you don’t want to own then when their prices go down.

3) Moral of the story–you don’t want to own bonds when people start worrying that inflation, and therefore interest rates, will go up.

There is a reason why I used tangible asset prices, like houses or gold bars, in this example rather than consumer goods prices, like the CPI. The logic of the analysis requires us to compare the total return of two assets after holding both for one year. That works fine for houses and gold bars because they don’t physically disappear during the year (they have low physical depreciation rates and low storage costs).

The analysis does not work, however, for haircuts, guitar lessons, or the other services that make of 70% of the market basket of goods used to construct the CPI. They disappear the moment you buy them. It doesn’t work well for popsicles, watermelons, or other nondurable consumer goods either. By implication, there is no reason to expect interest rates and CPI-based inflation measures to move together, despite what you read in the newspapers.

Dr. John

The views and opinions expressed in this article are those of Dr. John Rutledge. Assumptions made in the analysis are not reflective of the position of any entity other than Dr. Rutledge’s. The information contained in this document does not constitute a solicitation, offer or recommendation to purchase or sell any particular security or investment product, or to engage in any particular strategy or in any transaction. You should not rely on any information contained herein in making a decision with respect to an investment. You should not construe the contents of this document as legal, business or tax advice and should consult with your own attorney, business advisor and tax advisor as to the legal, business, tax and related matters related hereto.