Corrected October Inflation 1.5%

Summary: A string of October inflation reports confirms that inflation has come down much faster than the Fed thought possible. It is time for them to stop the FedSpeak, halt their QT program’s $95 billion of monthly bond and mortgage sales, and prepare to cut the Fed funds rate.

I have been arguing for months that the official CPI and PCE data the Fed uses to measure inflation have dramatically overstated inflation, which has led the Fed to push rates too high for too long. In recent days, a slew of October inflation reports confirms that inflation has fallen sharply and that it’s time for the Fed to reverse course. This note summarizes the recent inflation data.

This week’s October CPI report showed that consumer prices were flat for the month (0.0%) and were 3.2% higher than a year earlier. As I have written in previous posts, the index is dominated by so-called owners’ equivalent rent of residences, or OER, a wholly fictitious number that purports to measure the amount of rent every homeowner would have to pay if they were to rent their own home from themselves. I have written at length about why OER should be stricken from the index. Let’s look at the result if we were to do that.

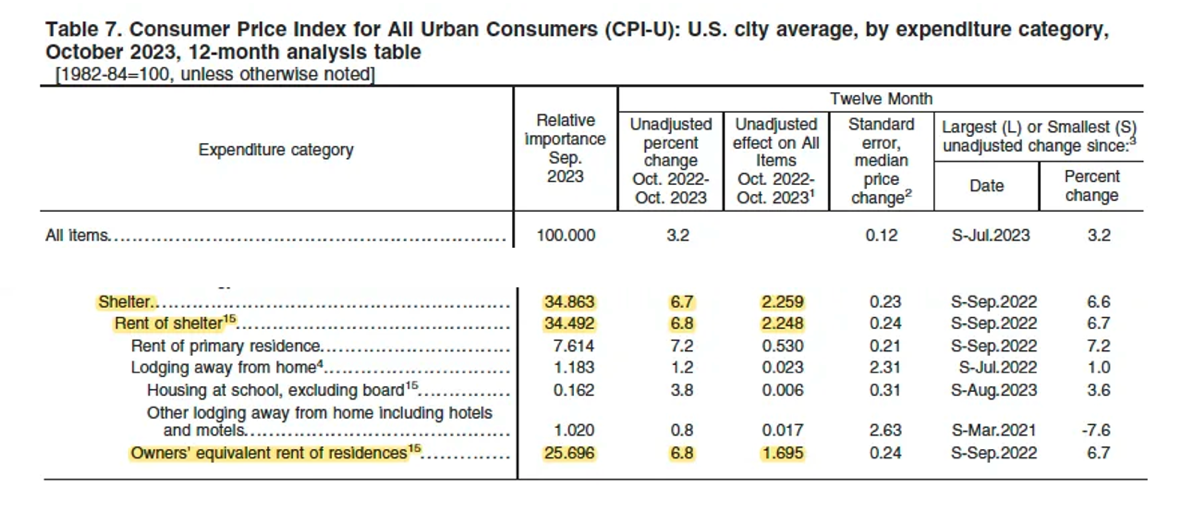

The table, above, taken from the October CPI report, shows the official All items number, up 3.2% over the previous 12 months, in the top row. The leftmost column shows the weight of various components of the market basket of goods and services used to construct the index. Shelter makes up 34.863% of the index. Of that figure, Rent of primary residence (rent paid by people who actually pay to rent their residences) accounts for just 7.614% of the index. This is a real, out-of-pocket expense paid by renters and belongs in the index. The rest, labelled Owners’ equivalent rent in the table, (the imaginary rent people supposedly pay to themselves) makes up a whopping 25.696% of the overall CPI index. It should be removed.

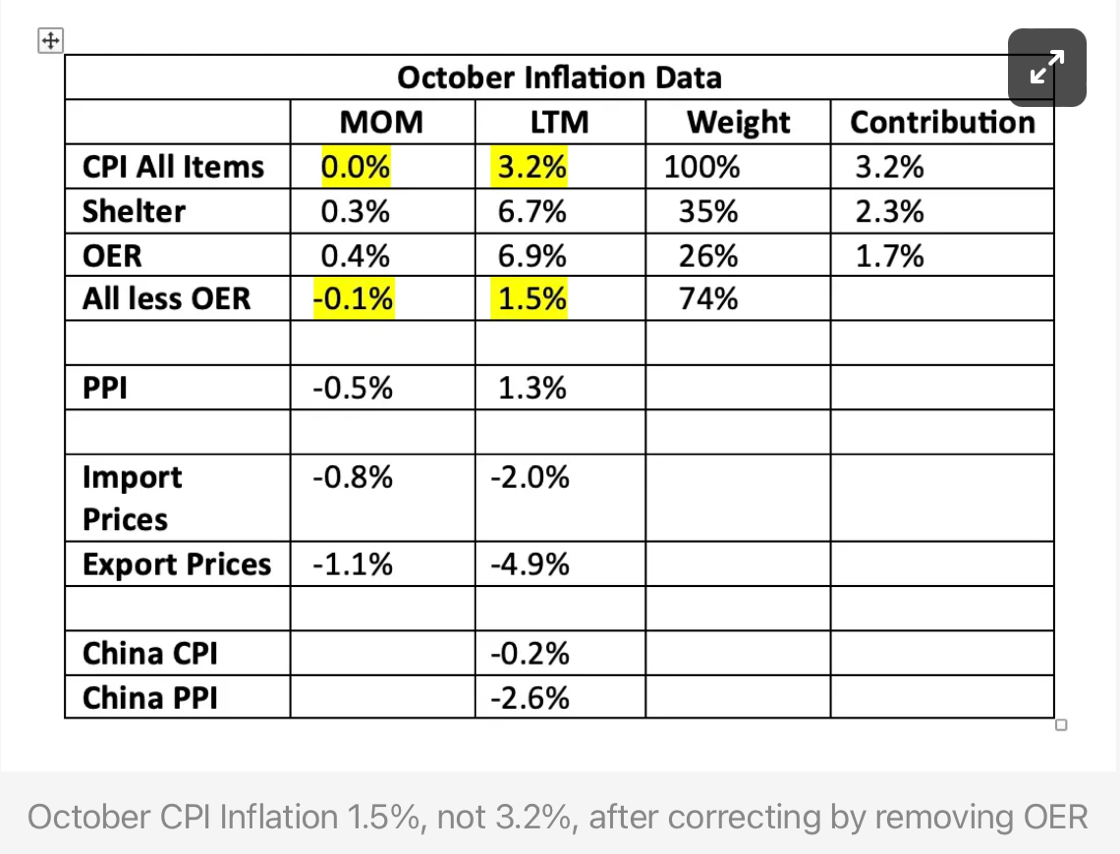

The table above shows the impact of OER on the October inflation figures. In the top row we see the reported numbers, 0.0% month-on-month (MOM) and 3.2% for the last twelve months (LTM). In the third row, you can see that OER, which makes up 26% of the index, rose 0.4% MOM and 6.9% LTM. In the fourth row, labelled All less OER you can see the result of excluding OER from the index. Instead of the numbers in the official report, inflation was -0.1% for the month and just 1.5% over the last twelve months, significantly below the Fed’s 2% inflation target. This is the number the Fed and investors should focus on.

Farther down the table you will see that the CPI result is not a fluke. October numbers for the PPI were -0.5% for the month and 1.3% LTM. We also see that October import and export inflation were below zero both MOM and LTM.

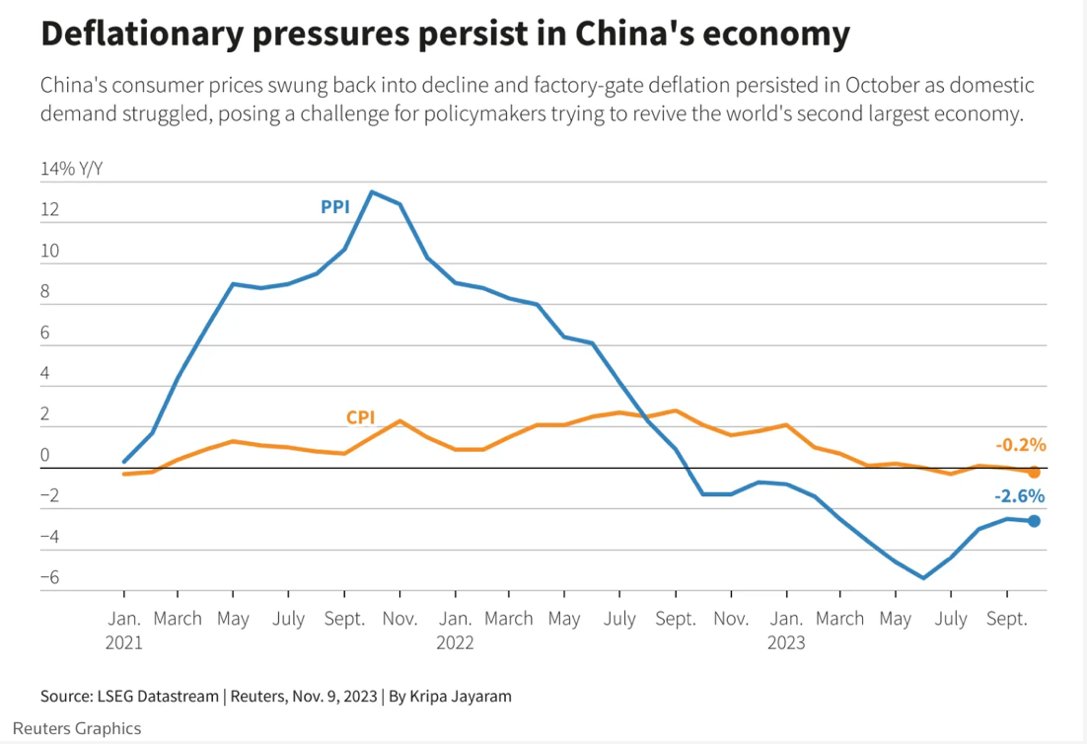

And it’s not just the US. China’s CPI and PPI inflation were both negative in October. And Chinese home prices in the 70 biggest cities fell by -0.4%.

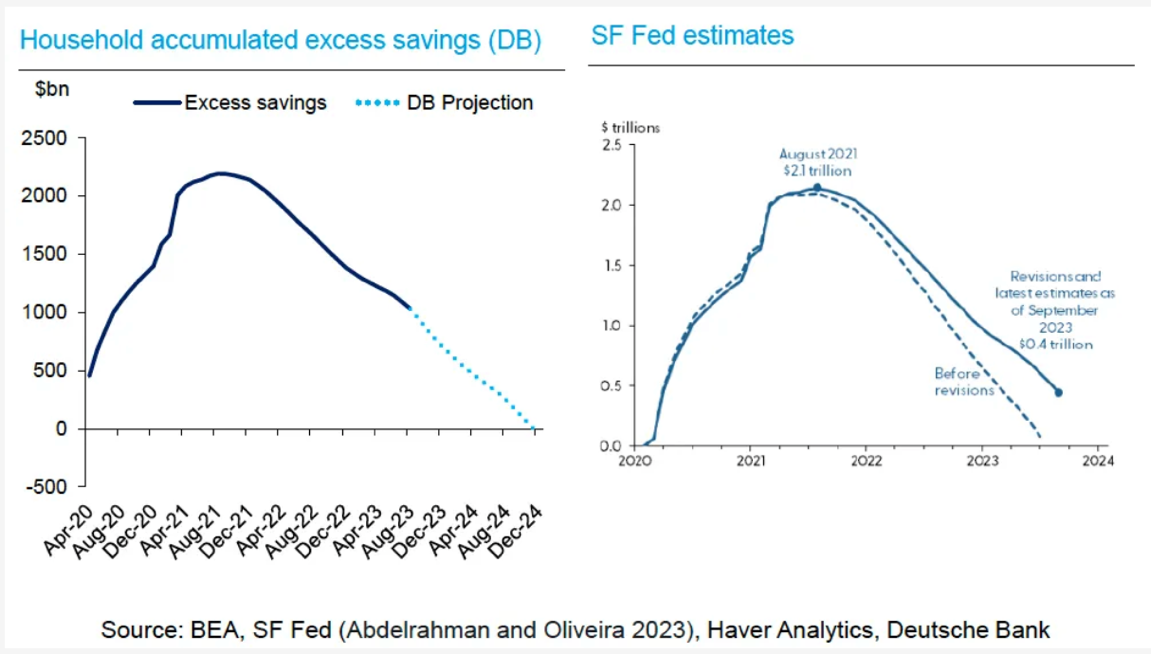

So far, the U.S. economy has continued to grow, thanks to the fact that American households are still burning through the excess cash they accumulated during the pandemic. But the projections, above, from Deutsche Bank and the San Francisco Fed suggest people will soon run out of firewood.

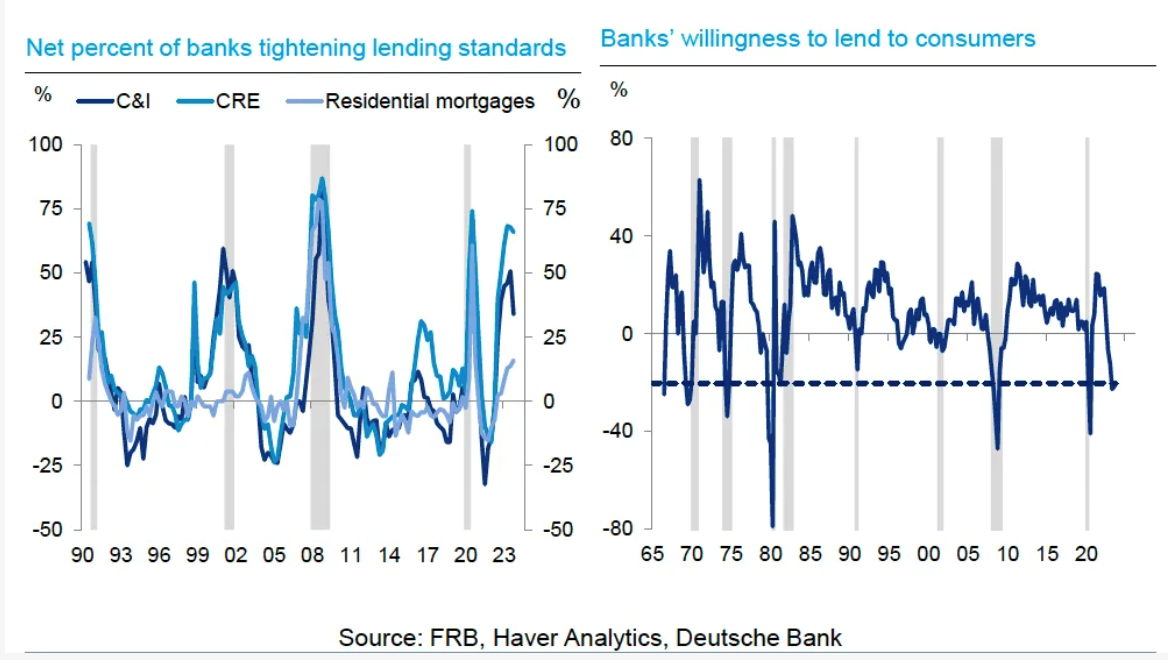

That, and the relentless tightening of lending standards (above) by banks weighed down by underwater Treasuries, MBS, and CRE loans make growth over the next year look not so good. Add the recent upward drift in jobless claims, the drop in commercial real estate values that won’t show up in the data until failed refinancings trigger forced selling in the next two years, and the downward drift of industrial production and you have plenty of reasons why the Fed should stop selling bonds now and begin the downward path in the Fed funds rate that everybody knows has to happen.

My advice for investors is unchanged from the last post. The weight of evidence is now clearly in the direction of lower rates, which is positive for both bonds and stock prices. But the real money is going to be made next year by being a buyer in the fire sales. Make sure you have plenty of cash on hand when we get there.

Dr. John

The views and opinions expressed in this article are those of Dr. John Rutledge. Assumptions made in the analysis are not reflective of the position of any entity other than Dr. Rutledge’s. The information contained in this document does not constitute a solicitation, offer or recommendation to purchase or sell any particular security or investment product, or to engage in any particular strategy or in any transaction. You should not rely on any information contained herein in making a decision with respect to an investment. You should not construe the contents of this document as legal, business or tax advice and should consult with your own attorney, business advisor and tax advisor as to the legal, business, tax and related matters related hereto.